What if a crypto currency or a native digital currency becomes the mainstream payment method? What can be the long-term impact on consumer finance?

A few days ago, Matt Levine included some thoughts on the impact of the Digital Yuan on Chinese and eventual global financial system in his daily newsletter. Hence, I started asking myself – what will financial life look like for an average Joe/Jane if a digital currency goes mainstream?

The goal of this post is to answer these (not so) simple questions.

Where we are today

The bank account is still the epicenter of the user’s financial life, for the majority of users. Until a recent past, the bank account’s role in the financial lifecycle of the user was overwhelming, as banks really represented the only interface to the financial system for a customer.

The Bank Account was the sun and a number of ancillary services were built around it.

Over the last 10 years, the situation changed significantly. There has been a relentless trend to migrate away from banking services to different players. Financial services went through a strong unbundling phase, and many domains don’t really belong to banks anymore: payments are not really controlled by banks anymore, shadow banking controls great chunks of the lending industry.

But even though banks’ business models are clearly under pressure, the bank account and its constellation are still considered the epicenter of the financial life of the user. And that is the reason why many fintech companies are trying to rebundle their user experience by becoming bank accounts providers (Transferwise, Revolut, Klarna, CashApp by Square).

The Impact on the existing financial system

Now, let’s assume that a digital-first currency becomes the dominant one in a specific geo (whether a single country, economic area or the entire world). I’m purposely ignoring whether this currency would be Bitcoin, Ethereum, Facebook Diem, Digital $/Yuan or a newly minted coin not yet invented.

This currency would have lots of nice properties, most of them inherited from its programmability, but, more importantly, it would allow the currency issuer to be connected directly to the user.

This means that every user in the system (either country/world) would sit on the same balance sheet. And this would have an enormous impact on their financial life.

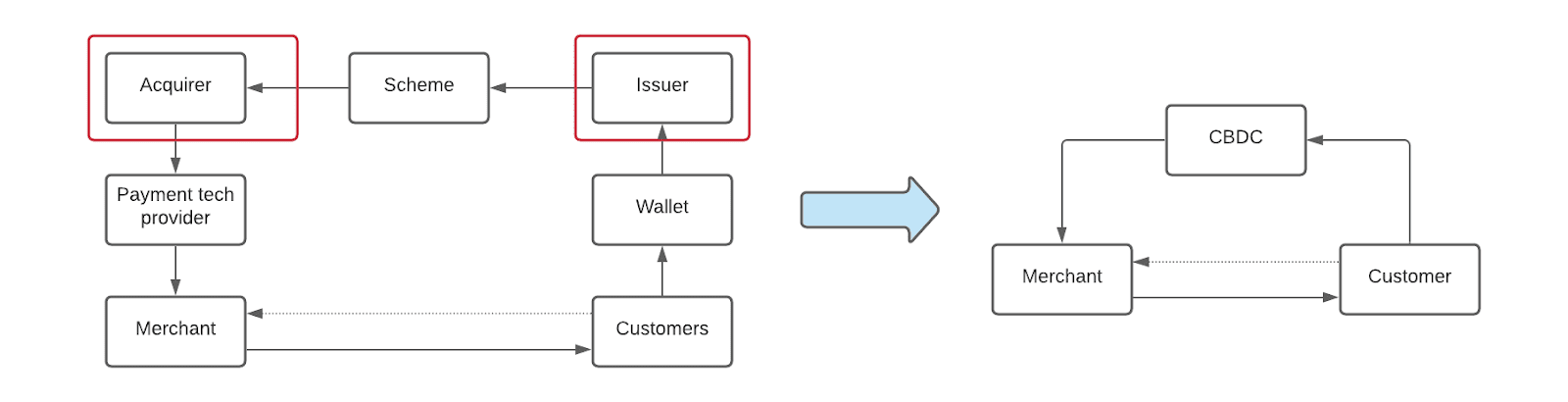

In this scenario, storing and moving value, essentially the basic use case of a bank account, would cease to exist. A user could easily do this activity through its cryptocoin or CBDC address.

Hypothetically then a user won’t really need a relation with a bank to perform basic financial needs like storing money, transferring funds or even paying in stores/online.

Banks would essentially lose a reason to exist for many people and, as a consequence, they would lose access to quasi-free capital, while foregoing their money marketplace nature to turn into pure loans origination machines.

A similar fate would affect schemes and payments companies. If the users (retail and business) are all sitting on this universal balance sheet, paying for some goods ends up in being a simple balance sheet entry, with no 3rd party risk at all.

Taken to its extremes, these developments could lead to the payment industry as we know it being virtually cut off from the financial life of a user. Account to account transactions would make financial intermediaries redundant.

On the other hand, even though the basic financial needs like storing and moving value will be provided by some protocols or centralized financial institutions, big opportunities would open up in more advanced financial needs. It is very unlikely indeed that a protocol/central bank would provide features like access to credit and investments, or more sophisticated versions of these.

Positioning in a new system

A dominant CBDC/crypto protocol is nothing else than another attack to the existing business models of the financial system, the featurization of the core use cases of banks and payment companies: deposits and money transfer. But it is a very hard hit, because it attacks the fundamental relation between the users and the financial institutions, probably the core reasons behind using these companies.

If a financial company wants to survive in a digital-first currency financial world, providing a semi-commoditized financial functionality at scale won’t be an option anymore, as the commoditized financial feature will be provided by the system itself.

Financial institutions will have to position themselves differently. Here are two ideas to spark the (futuristic) conversation:

Money button on the smartphone – become the aggregator of the financial life of the user. In this sense the fintech company / bank app would be more an engagement app than a financial one: it would win through a marvelous customer experience where it manages to engage the user and it would orchestrate a plethora of services and ecosystems, providing an extra value than just the sum of them.

As I don’t expect that a native digital currency will wipe out the existing system and multiple financial systems will coexist, the need for an experiences’ aggregator will grow stronger.

If it is already complex today to keep finances under control with an app for trading, one or two bank accounts, a savings app and maybe a personal finance app – I imagine this pain would grow 10x if we add the financial ecosystem variable to the picture.

A highly automated personal finance buddy will be essential to coordinate and harmonize the constellations of specialized services among various ecosystems: traditional bank accounts, CBDC world, cryptocurrencies ecosystem, embedded financial products.

Infrastructure provider – The alternative to becoming super-aggregator apps is to focus on a specialized niche and move down the stack to become a service provider of some sort, something that I already described in my previous post.

This is a feasible alternative but these providers will mainly be tech providers more than financial ones, something that doesn’t really resonate with the skillsets of incumbent financial companies.

Conclusions

I believe that the advent of a dominant native digital currency is only a matter of WHEN, not of IF.

Timing innovation is very hard but all the pieces are there to demonstrate that the current monetary solution doesn’t work, and eventually a monetary crisis will move us towards a new financial system.

To thrive in this new system, financial companies will have to focus on a universal business concept: understand their users needs and forget about the solution that served them for 30 years. It’s probably the only way to survive.