If you have been reading this blog for some time, you know that I’m very bullish on DeFi and its applications. I’ve been actively following the space since 2018 and I have been impressed by the speed of iteration and growth throughout multiple verticals.

Given my previous experiences building lending products, I’ve followed even more closely the projects that were working on lending and credit: Maker Dao, Aave, Compound.

These projects, which experienced insane growth over the last 2 years, are characterized by a very simple interaction model: the user deposits some tokens as collateral in exchange for a loan of another token type. For example I can deposit some Eths as collateral and get a loan of DAIs.

From a consumer perspective, this is not really a loan: the average Joe/Jane usually asks for a loan when they need liquidity quickly and leave some form of illiquid guarantee in exchange (more on this later). Those DeFi services don’t really generate liquidity in the traditional sense, but they act more as pawn shops where users deposit a liquid asset of a certain type, to get a loan of another liquid asset.

Today’s main use cases are essentially two:

- GROW CRYPTO WEALTH – the user wants to increase exposure to crypto assets or execute some trading strategy

- REMAIN IN THE CRYPTO SPACE – the user needs some liquidity off-chain but wants to remain in the crypto space and doesn’t want to sell their crypto

Both use cases proved to be incredibly successful. And yet if DeFi really wants to expand to the masses, lending projects will have to evolve and start serving another major use case: solving liquidity issues by leveraging less liquid assets like reputation and real world assets.

How real world lending works

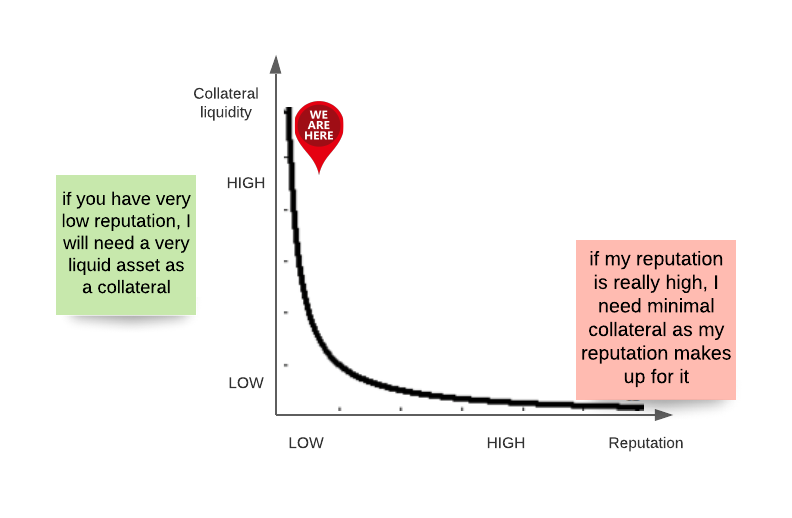

In the physical world, borrowers often ask for a loan when they have liquidity needs: for example, they can’t make some short term payment and thus they ask a financial institution for a loan that they guarantee they will pay back. This guarantee is underpinned by some less liquid collaterals: Reputation, Assets or both.

Those two assets will then be hypothecated by the lender and claimed in case the loan defaults. The loans can still be overcollateralized, but with less liquid assets (real estate, car) or can be undercollateralized and guaranteed by an intangible asset (the borrower’s reputation in the form of a credit scoring).

The situation in crypto today is very different: loans are all overcollateralized – so the value of the collateral is higher than the value of the loan – and are also guaranteed by a very liquid collateral – another crypto token. This kind of scenario is necessary for multiple reasons: in first place, there is no straightforward way to establish the reputation of the borrower on-chain; secondly, there is a very limited token representation of any real world assets on-chain.

Consequently, the only option for the lender is to require crypto-tokens – a liquid asset – as future guarantee of the repayment of the debt.

Reputation

If DeFi lending wants to expand beyond traders and crypto-fans, the logic of the real world will have to filter into the crypto space, and find its own original adaptation there. For instance, loans may be offered not only on the basis of the liquid collateral provided, but also on the reputation of the borrower.

Today DeFi applications assume that the user has 0 reputation, mainly because they were developed around a pseudonymous ecosystem. For this reason they have to ask for liquid tokens as collateral, as there is no other way to enforce the future collection of the loan in case of default.

However, this is already changing. A first wave of projects working on this new collateral dimension is emerging. These companies are taking complementary approaches to add the reputational dimension to loans: some companies are trying to channel off-chain reputation into the on-chain world, other projects are actually trying to directly build a reputation system on-chain.

On the first front, companies are essentially trying to use the reputation that the user built in their off-chain lives, but to collateralise on-chain loans. The most interesting examples are Goldfinch and Teller.

Goldfinch is actually working to implement a decentralized loan underwriting protocol that will allow anyone in the world to become an underwriter (using data available to them) and use this information to issue loans on-chain. The idea is to gather pieces of data produced both in the corporeal life and in the virtual life, and leverage them to build a reputation of the user, that can be applied on-chain.

Teller is taking a more centralized approach: they integrated Open Banking solutions and are actually using loan applicants’ bank transactions to estimate the creditworthiness of the user – but using credit models that are approved by a decentralised community.

On the second front, multiple projects are building a federated identity directly online: these companies are trying to establish an online reputation and to make it available to service with various purposes. The main examples are Spruce_ID, IDX, Decentr.net and Bright_ID.

An even more extreme approach is presented by “on-chain only reputation” providers, like Degenscore or ARCx Sapphire.

ARCx Sapphire is a DeFi project that creates a DeFi passport for the user’s wallet, providing a scoring assessment built on the on-chain financial life of the user.

The Degenscore does a similar job, but focuses only on the level of financial Degeneration of the user – degens are a DeFi subculture associated with a highly speculative approach of the user. Degenscore essentially measures the speculation activity of a user and summarizes it in a number.

Both applications, that today are relevant only for a small niche, can eventually evolve into one of the fundamental primitives of the DeFi system, when more and more elements of the financial life of the user will be migrated on-chain.

Real world assets (RWA)

The second key dimension that has to be introduced to seriously expand the adoption of DeFi loans is real world assets as collaterals. Not everyone has on-chain tokenized assets and certainly not the majority of people who could be interested in borrowing assets to access liquidity.

The typical example here is the most common lending product around: the mortgage. A mortgage is an overcollateralized loan where the property acts as a collateral.

The borrower picks a house to buy, uses it as a collateral together with his/hers reputation to get money needed to pay the house from the bank. The borrower will then pay the loan back little by little or – in case of default – the bank will claim ownership of the house.

This very common product is currently unsupported at scale by DeFi. But things are moving.

The most active players in the DeFi space, seeking to expand towards real world asset acceptance, have been MakerDao and Centrifuge.

MakerDao is taking more and more the role of a system credit engine. The Maker’s community has voted to accept real world assets as collateral for their DAI loans, a decision that is moving them to become a universal credit facility of the DeFi space.

Centrifuge is working more to become the securitisation layer that bridges the gap between real world and defi. In particular, their front-end application Tinlake allows real world asset originators to borrow DAIs using their real world assets.

RWA originators will issue NFT tokens that represent the real world asset on the Ethereum chain through the Centrifuge protocol. These NFT tokens will then be pooled into the Tinlake pool – a sort of SPV – which investors can also access.

RWA originators will be able to borrow DAI from investors in this pool, collateralizing the loans with the NFTs.

This process allows borrowers to instantaneously turn off-chain assets into liquidity and guarantees new investment opportunities for lenders.

Today various real world asset originators have built a pool on Tinlake, getting to over $ 18M of originated loans. These numbers are still insignificant numbers if compared to the global lending market and even to the DeFi loans originations but I am convinced that this is the very beginning of a completely new way of distributing credit and originating lending assets. These processes will likely become the standard in lending over the next decade.

Conclusion

I’m firmly convinced that DeFi represents the obvious evolution of finance. It will add transparency, speed and efficiency to a traditional financial system that is discretionary, permissioned, and opaque.

The key to making this transition happen is to open up new use cases, delivering the value that blockchain unlocks to the millions of people using credit products every day.

This will be impossible if some established and very convenient features – like using your reputation or a real world asset to get credit – are not natively integrated in new paradigms. Luckily, lots of great projects are already here to build them.

Thanks to Yannick for his kindly review of the essay.

Resources

Reputation

- TheDefiant on Decentralized reputation – LINK

- Tearsheet of Decentralized credit scoring – LINK

- Jill Carlson on Decentralized credit scoring – LINK

- Goldfinch – LINK

- Teller Finance – LINK

- TrueFi – LINK

- ARCx Sapphire – LINK

- Degenscore – LINK

Real World Assets: