The first part of this year the crypto space has been characterized by a sudden and – in many cases – unexpected, bull market. Prices returned to all-time highs very quickly, and the most important narrative fuelling this phenomenon is staking, particularly through its most advanced evolution, which is restaking.

The goal of this post is to explain to a non-crypto user what staking is, how it has evolved over the years, and to analyze its adoption as a more mainstream source of yield.

What staking is?

Digging deeper below the surface of the constant hype machine that is the crypto industry, there are ultimately three organic sources of yields, i.e. three forms of capital deployment that produce a return: lending, funding rates, and staking.

Lending involves loaning your crypto assets to others through various platforms and receiving interest, generally determined by the market, in return.

Funding rates refer to the payments made between traders in perpetual futures contracts. Those who are long (buying the futures) may pay those who are short (selling the futures), and vice versa, depending on the relative positions and market conditions.

Staking is the process of participating in transaction validation on a blockchain and receiving rewards in return.

In particular, staking is the job of securing a Proof of Stake blockchain (like Ethereum) through the native assets of the chain itself: the staker (also referred to as validator in this context) locks a certain amount of crypto tokens in a wallet to support the operations of a network. Those crypto tokens are at stake: if the node doesn’t follow the guidance of the network and doesn’t act as expected, the tokens are confiscated (or ‘slashed’ in crypto jargon). Not following the rules means violating the consensus mechanism of the chain, which essentially means introducing malicious transactions to the blockchain. If the validator acts appropriately, they receive in return rewards from the blockchain, in the form of extra crypto tokens of the blockchain itself.

Staking evolution

Staking was invented in 2012 with the introduction of proof-of-stake consensus by the Peercoin project, with the goal to replace the energy-intensive proof-of-work approach that characterized blockchain operations thus far. Proof of Work (PoW) relies on miners competing to solve complex puzzles with powerful computers, with rewards given to the first successful miner. In contrast, Proof of Stake (PoS) operates like a lottery, where the likelihood of being chosen to validate transactions increases with the amount of cryptocurrency held and staked as collateral, eliminating the need for energy-intensive computational competition. PoS offers a more energy-efficient alternative to PoW, promoting greater accessibility and participation in blockchain networks.

The initial staking providers were essentially individuals that were running validators and staking their own coins. As the crypto space became more crowded and professionalized, requirements to stake grew, and individuals faced bigger hurdles. This triggered the emergence of pooled staking services like Rocket Pool or Staked: users could aggregate their crypto tokens with participants in shared pools that met staking requirements.

With pooled staking, the accessibility problem to staking was partially solved, but concerns about liquidity remained as many participants noted the locked nature of their staked cryptos. This led to another innovation that drastically changed the staking space: the introduction of liquid staking. With liquid staking, launched and popularized by Lido Finance in 2020, protocols returned a receipt token that represented the assets staked. This receipt token (i.e., Lido’s stEth) could be freely traded and used across the DeFi ecosystem, while staked tokens were still accruing a return for their staking activities. Liquid staking lowered the barrier to entry to the market, it brought liquidity to token staking, and removed many constraints of withdrawal.

Over the last six months, a new frontier of staking rose to popularity: restaking, popularized by EigenLayer. Restaking consists of reusing staked crypto tokens (Eth to begin with) to secure other applications within the ecosystem. In a nutshell: already staked ETH are used by EigenLayer to extend crypto-economic security to support other applications. EigenLayer basically offers protocols the opportunity to tap into Ethereum’s security layer, enabling them to access a larger set of validators and improve their initial security (Security-as-a-service for Dapps). This allows validators to earn extra rewards of course with extra slashing risks.

Staking as an investment class

Given the fairly low volatility of the rewards rate provided by blockchains, Staking has become a major asset class in crypto with many players offering staking-as-a-service solutions to both institutional and retail players. All the main centralized exchanges (Binance, Coinbase, KuCoin, Kraken, Crypto.com, and many others) offer a staking-as-a-service solution for the clients that custody their crypto in their wallets. On the institutional side, players like Figment, Staked, and Restake.net are purely staking-centric, but also crypto institutional custodians like Fireblocks or Blockdaemon are offering their staking-as-a-service solution. In the Decentralized Finance space, Lido Finance is by far the most important staking player with approximately $30B locked. However, its relentless growth has seen a halt since the go-live of EigenLayer and its highly aggressive ecosystem.

As mentioned in the beginning, structured products have also been built on top of staking solutions. The most popular right now is Ethena, a service that essentially allows access to enhanced staking rewards via stablecoins – more on Ethena and its yield here.

Open points

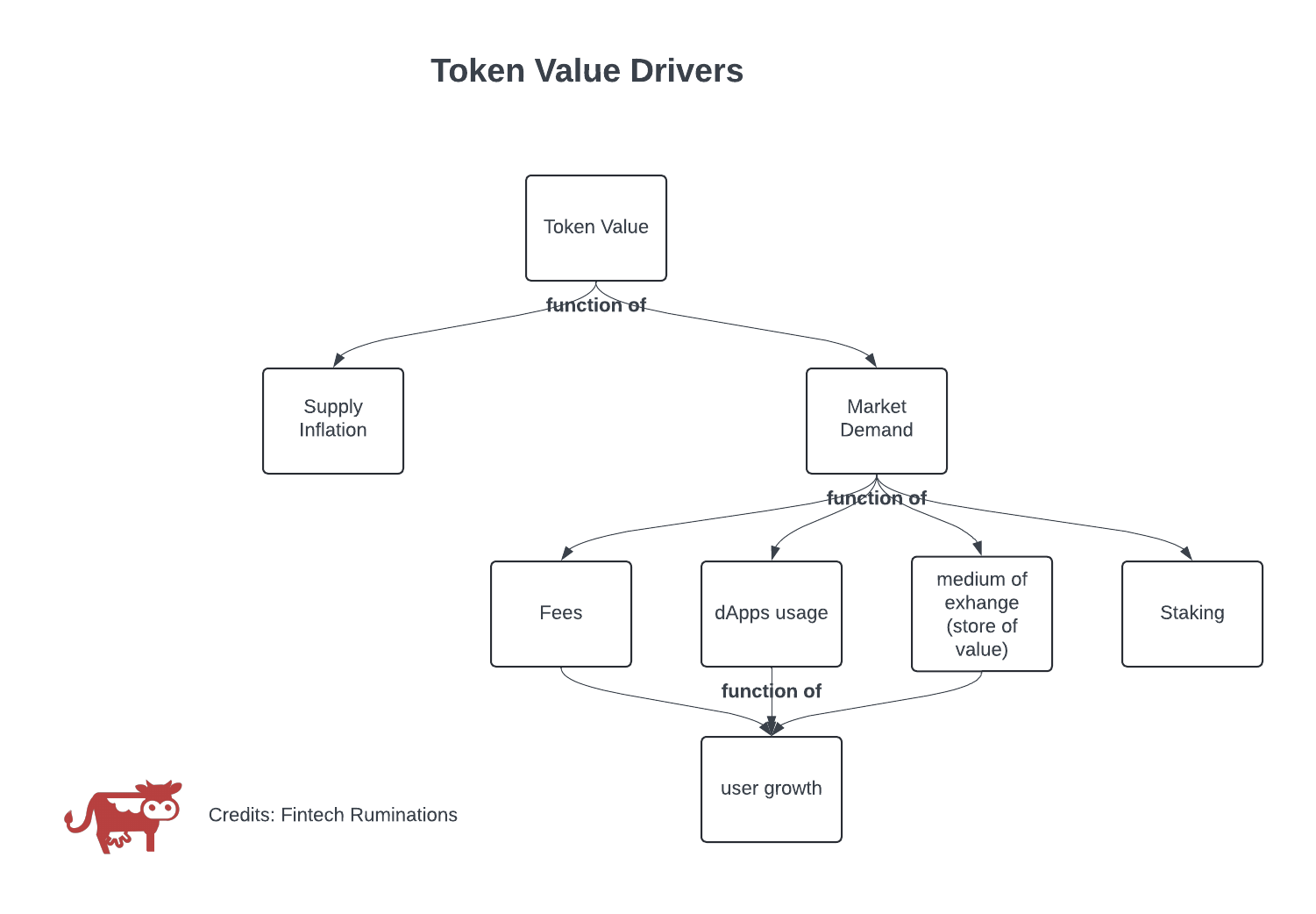

Staking has been tremendously successful so far, but the key driver to long-term sustainability is token value appreciation or, at least, stability. The token being staked must retain or appreciate in value; if the token loses value, so do the rewards, which are issued in the form of the token itself.

In order to retain value, the token must consider two key factors: supply inflation and, more importantly, demand for the token itself.

The token supply inflation must be well balanced, new tokens created must not lead to excessive inflation that may collapse the value. So new token issuance must be balanced with the market demand.

The market demand for the tokens comes actually from the usage of the token itself either in dapps, in fees, or as a medium of exchange and store of value. All three components depend on user growth, so ultimately the market demand is a function of the chain adoption, and growth is linked to users and use cases.

The growth of staking will also be inevitably linked to its regulatory status. As most of the crypto world, staking stands in an ambiguous position, particularly in the US, where the SEC has opened a complaint against Coinbase for its staking-as-a-service offering, after the settlement of a previous similar case against Kraken.

From the SEC perspective staking products are securities as they fully pass the “Howey Test” – the legal framework outlined by the U.S. Supreme Court to determine whether a transaction qualifies as an investment contract and should be regulated. For the SEC staking is an investment of money, in a common enterprise with an expectation of profits produced primarily from the efforts of others.

Coinbase challenges this version, supporting the thesis that staking is close to mining – which has been considered not a security in multiple rulings – and pushing back on each single point of the Howey Test.

It is not within my skill set to speculate which will be the decision on this case, but this decision will probably influence the short term evolution and adoption of staking, given the size of the US capital market and its centrality to the global financial system, even though I do believe that in the long run, things will not be really affected.

Conclusions

Staking is the hottest thing in crypto right now.

The most controversial projects of the new bull run – Ethena and EigenLayer – are developed around staking. Funds fully dedicated to investing in staking rewards have just launched – Greyscale Dynamic Income Fund a few days ago. Staking performance website aggregators – like Staking Rewards – are emerging.

I’m convinced that, regardless of the SEC decision, staking as a yield opportunity is here to stay, and I do believe that it will inevitably grow as public PoS blockchains will be adopted more and more.

RESOURCES

- State of Staking by Staked – link

- Staking: Security or Not